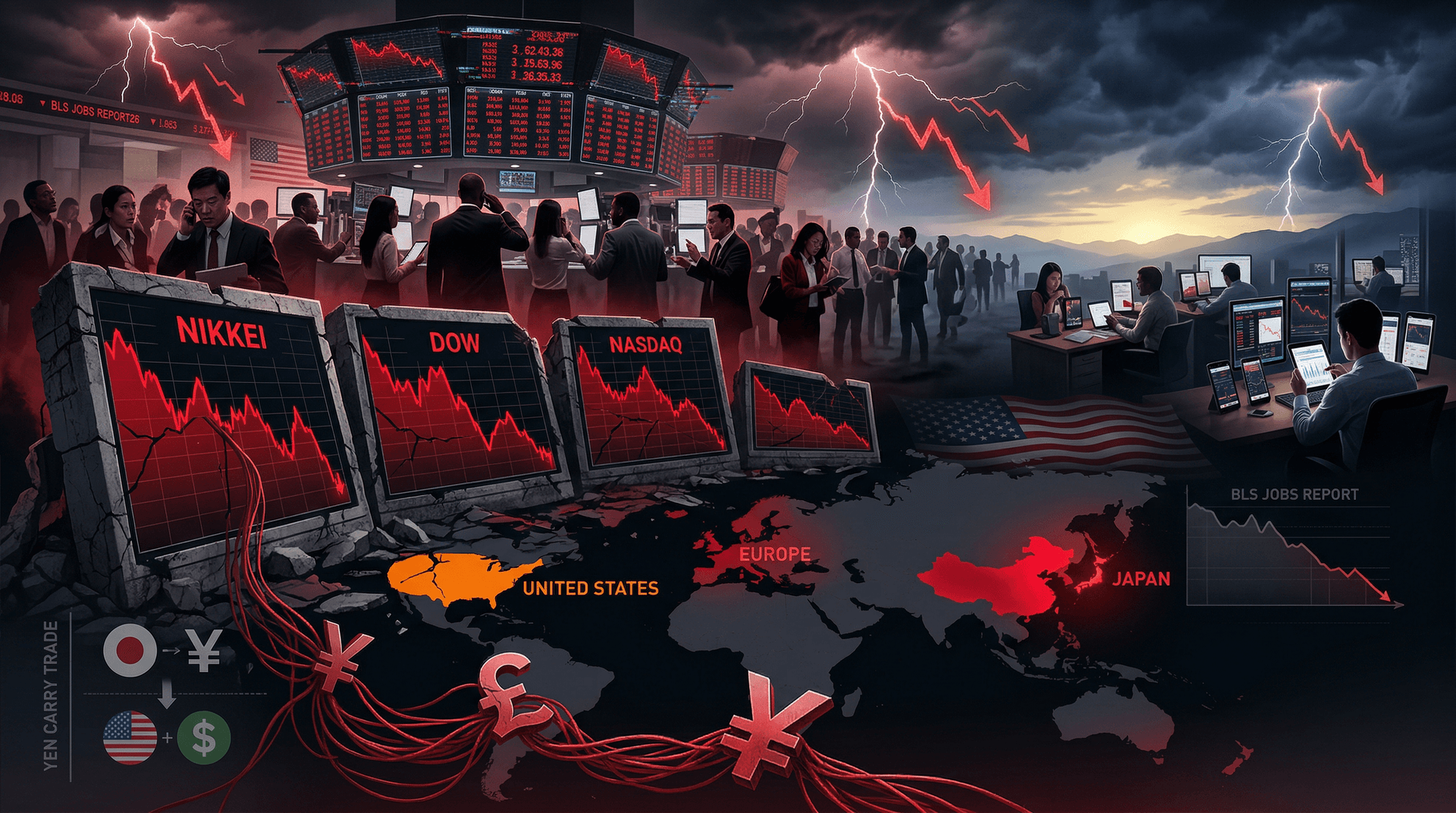

In a stunning display of market volatility, global stock exchanges convulsed on August 5, 2024, marking the most severe single-day losses since the early COVID-19 panic in March 2020. Japan's Nikkei 225 index plummeted 12.4%, its largest drop since Black Monday in 1987, wiping out over $4 trillion in value across Asian markets alone. The Dow Jones Industrial Average futures tumbled more than 1,000 points pre-market, while Europe's STOXX 600 fell sharply at open. This chaos was ignited by a disappointing U.S. July jobs report, which showed only 114,000 jobs added—far below expectations—and unemployment ticking up to 4.3%.

The Spark: U.S. Jobs Data Disappoints

The Bureau of Labor Statistics (BLS) report, released on August 2 but fully digested over the holiday-shortened week, painted a picture of a cooling U.S. economy. Revisions shaved 86,000 jobs from prior months, signaling deeper weakness. Economists had anticipated 175,000 new positions, but the shortfall fueled fears that the Federal Reserve's aggressive rate hikes since 2022 had finally bitten too hard. "This is the canary in the coal mine for recession," noted Mark Zandi, chief economist at Moody's Analytics, in a post-report interview.

From a diverse array of viewpoints, the data highlighted inequities. Black and Hispanic unemployment rates rose disproportionately, underscoring persistent labor market disparities amid economic slowdowns. Women, who have re-entered the workforce in record numbers post-pandemic, faced added pressures as service-sector jobs—often held by underrepresented groups—bore the brunt of cuts.

Domino Effect: Yen Carry Trade Unravels

The sell-off cascaded globally, amplified by the unwinding of the yen carry trade. For years, investors borrowed cheap yen to fund high-yield investments in U.S. tech stocks and other assets. Japan's rate hike to 0.25% on July 31 strengthened the yen by 14% against the dollar in a month, forcing leveraged positions to liquidate en masse. This "dash for cash," reminiscent of 2008, hit tech-heavy indices hard.

Taiwan's Taiex index cratered 9.8%, dragging down semiconductor giants like TSMC, vital to the global chip supply chain. In Europe, banks like Deutsche Bank shed 5-7%, while luxury goods firms—proxies for consumer spending—tanked. U.S. tech titans weren't spared: Nasdaq futures pointed to a 4% drop, with Nvidia and Apple sliding in after-hours trading on fears of curtailed AI spending if recession hits.

Impacts Across Economies and Demographics

The plunge resonated differently across the globe, reflecting inclusive perspectives on economic interconnectedness. In Japan, retail investors—many middle-aged savers relying on stocks for retirement—saw lifetimes of gains evaporate. Women, who comprise a growing share of Japan's individual investors (up 20% since 2020 per Nikkei data), were particularly vulnerable, as cultural shifts toward financial independence clashed with market mayhem.

Emerging markets offered a counterpoint. India's Sensex dipped modestly at 2%, buoyed by domestic resilience and less exposure to carry trades. African exchanges like Nigeria's NSE fell under 1%, but analysts warned of spillover via commodity prices—oil dipped below $70/barrel, hurting exporters. In Latin America, Brazil's Bovespa dropped 2.5%, with diverse voices from favela entrepreneurs highlighting risks to micro-businesses dependent on global trade.

Retail investors worldwide, empowered by apps like Robinhood and eToro, felt the sting acutely. A diverse cohort—Gen Z, millennials, and first-time investors from underrepresented communities—poured $1.5 trillion into U.S. stocks since 2020. Platforms reported surged activity on August 5, but with panic selling. "This tests the inclusivity of democratized investing," said Dr. Aisha Rahman, a finance professor at Howard University, emphasizing education gaps for minority investors.

Big Tech, a cornerstone of modern portfolios, bore significant losses. The "Magnificent Seven" (Apple, Microsoft, Nvidia, etc.) shed $500 billion in a day, questioning the sustainability of AI hype amid economic headwinds. Cloud providers like Amazon Web Services face scrutiny if corporate belt-tightening curbs capex.

Broader Implications for Business and Policy

From Wall Street to Main Street, the crash underscores fragility. Institutional investors, including pension funds serving diverse populations, scrambled to rebalance. BlackRock's Larry Fink warned of "synchronized downturn risks" in recent letters, urging diversified portfolios.

Central banks face pivotal choices. The Fed, under Jerome Powell, signals September rate cuts, but markets now price in 100 basis points by year-end—double prior bets. The Bank of Japan (BOJ) paused hikes, stabilizing the yen somewhat by August 6. Europe's ECB, already cutting, may accelerate.

Inclusive policies gain traction. Initiatives like the U.S. Women's Business Ownership Act expansions aim to shield minority entrepreneurs. Globally, calls grow for "equitable recovery" frameworks, integrating ESG factors to protect vulnerable sectors.

Outlook: Storm or Reset?

As markets stabilized marginally on August 6—Nikkei up 10% in a historic rebound—optimists see a healthy reset. Valuations, stretched at 30x earnings for S&P 500 tech, normalize. Recession odds, per JPMorgan, rose to 60%, but soft landing remains possible with Fed action.

For tech and finance sectors, this tests resilience. AI investments may pause, but long-term trends endure. Diverse investors, from Tokyo housewives to Nairobi traders, remind us markets are human endeavors—flawed, interconnected, and adaptable.

In Uchatoo's view, embracing multifaceted perspectives fosters better navigation. Monitor Fed minutes on August 8 for clues. Volatility persists, but history favors the prepared.

Word count: 912